Buy now, pay later in South Africa: what stores should know

Summary: This post explains what South African retailers should know about BNPL. It covers benefits, risks, and the impact on conversion.

Alternative payment methods are becoming increasingly important for merchants as South Africans become more comfortable with and interested in trying new payment methods. Our recent consumer report showed 90% of South African consumers have tried a new payment method in the last year alone.

Among these is Buy Now, Pay Later (BNPL).

The Buy Now, Pay Later market in South Africa is projected to grow by 13.6% annually, reaching $815.1 million in 2025 and set to exceed $1 billion within five years. Our research shows that 45% of respondents have used BNPL for everyday purchases – a clear sign that it’s moving from a niche to a mainstream payment option. This is particularly true for retail purchases with a higher value, indicating that this has the potential to increase overall basket size.

For merchants, this isn’t just about offering another payment method. To meet customers where they are, merchants need to offer BNPL as a payment method. When they do, they maximise opportunities to convert higher sales, strengthen brand loyalty and future-proof their checkout experience.

What is BNPL?

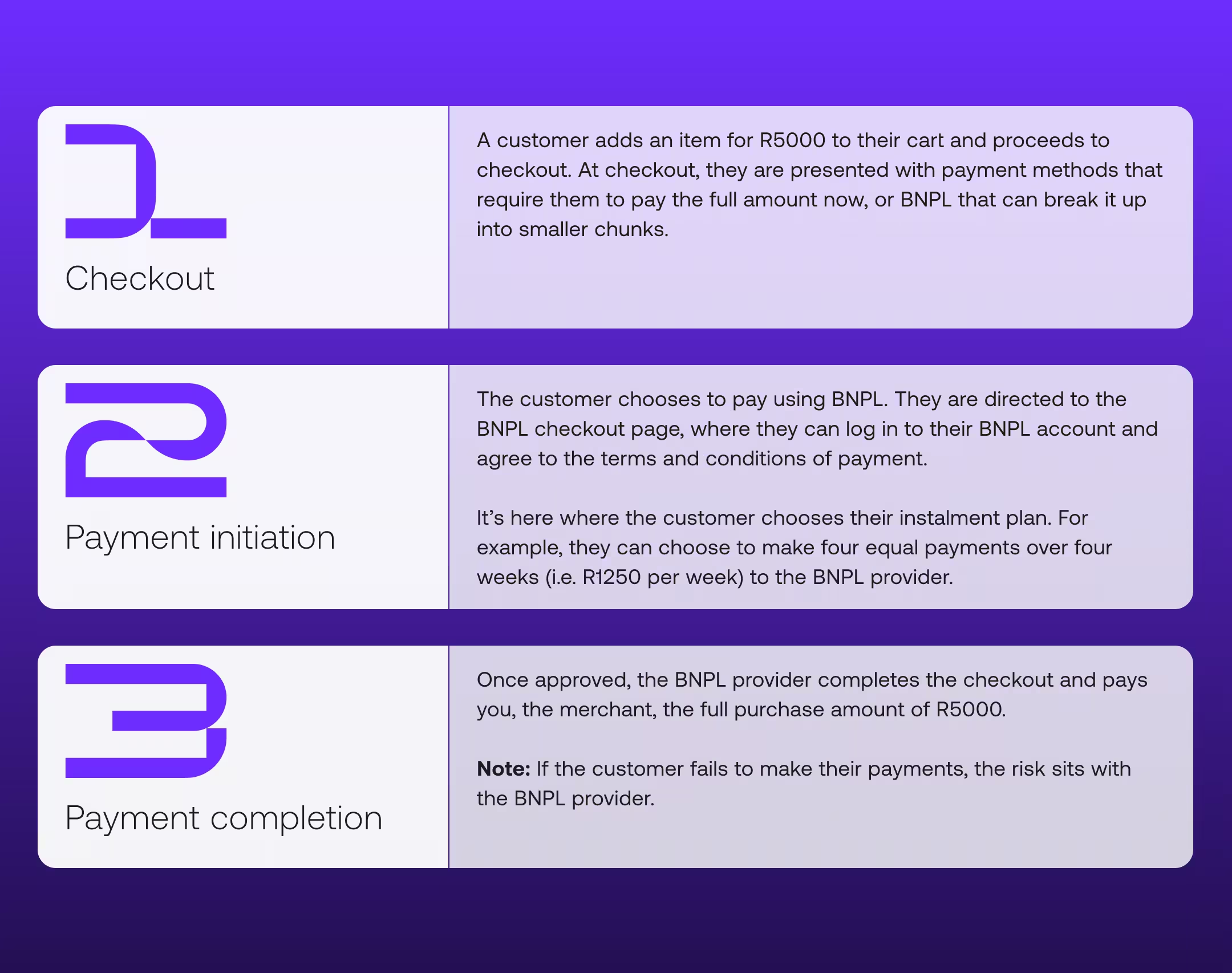

BNPL is a payment method that allows customers to pay with interest-free instalments instead of paying the entire amount upfront. The merchant receives the full purchase amount from the BNPL provider while the customer pays the BNPL provider over a short period (typically 2 weeks for smaller purchases to 12-24 months for larger ones).

BNPL services offer customers flexibility that helps merchants grow revenue from increased basket sizes and higher completion rates.

How does BNPL work?

When do businesses receive funds and associated fees?

Businesses can receive funds within 24 hours or up to a week, depending on the service provider you choose to integrate with. Service fees vary depending on the BNPL provider.

How does integration work?

Local providers like HappyPay, Payflex, Float and PayJustNow provide merchants with their plugin or API that integrates with ecommerce platforms like Shopify, WooCommerce and Magento.

Merchants with Stitch Express accounts can easily enable HappyPay on their dashboards.

How does BNPL differ from credit cards?

Credit cards rely on traditional credit scoring and often charge interest if balances aren’t cleared monthly. BNPL services usually offer short-term, interest-free instalment plans with only a soft credit check, making them more accessible for customers.

How businesses can benefit from BNPL

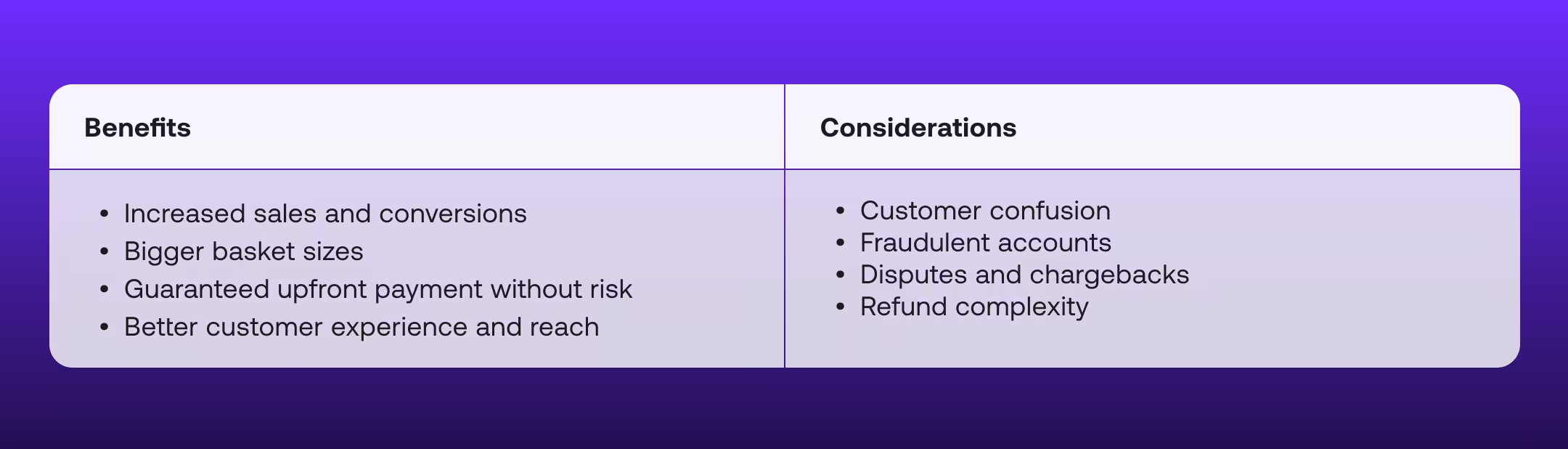

For merchants, offering BNPL comes with clear benefits that can directly boost sales and customer satisfaction:

Drives increased sales conversions

BNPL gives customers more flexible ways to pay, making them less likely to abandon their carts and more likely to complete purchases. It is estimated that it could boost conversion rates by 20% to 30%.

Increases average order value (AOV)

BNPL increases the customer’s spending power. Industry experts say that BNPL can increase the order size by 50%. In South Africa, uptake is strong amongst mid-high income earners who leverage the service for larger purchases.

Guarantees upfront payment, without the risk

Merchants receive their full payment upfront while the provider takes on the risk of collecting instalments.

Better customer experience and reach

BNPL gives shoppers the flexibility to pay in a way that suits them, creating a smoother, more positive checkout experience. At the same time, it opens the door to new customer segments that likely wouldn’t have converted without the instalment plan.

What businesses should consider

While merchants don’t carry credit risk with BNPL payments, there are operational processes to consider to protect revenue and customer loyalty.

Lack of customer education

This payment method is relatively new to many, so customers may not realise the merchant isn’t responsible for instalment collection. To avoid this:

- Clearly explain how instalments work before checkout.

- Add a clickable link to BNPL terms at checkout and in confirmation emails.

- Provide a link to the BNPL provider’s account portal so customers can track or manage payments.

- Partner with BNPLs that have strong onboarding and transparent checkout flows.

Fraudulent accounts and transactions

Fraudsters may use stolen or fake identities to make purchases, leaving merchants exposed to disputes after fulfilling orders. If BNPL instalments are funded by card, Stitch reduces this risk by authenticating all online card transactions with 3D Secure at checkout.

Managing disputes and chargebacks

BNPL providers mediate disputes between shoppers and businesses, but merchants must supply evidence to prove transactions were valid. Ensure your systems can provide delivery confirmation, transaction logs, and order details, just as you would in a bank dispute.

Processing refunds

Refunds can be sensitive, especially for first-time BNPL users. Delays or unclear processes may damage customer trust. To avoid this:

- Confirm your BNPL provider’s refund turnaround times.

- Make sure you understand how reconciliation works to maintain an accurate view of balances.

With Stitch Express, merchants can track BNPL payments directly in their dashboard. Transactions are clearly labelled for reconciliation, and balances are updated weekly with aggregated payouts for consistent cash flow.

Summary of benefits and considerations for merchants using BNPL

What are the best BNPL services to use in South Africa?

There are several providers offering BNPL services in South Africa. Merchants can choose from: Payflex, PayJustNow, MoreTyme and HappyPay to name a few.

What makes HappyPay stand out is its seamless integration with Stitch Express BNPL. Merchants can activate it directly from their Stitch Express dashboard, removing all the heavy lifting. Stitch Express offers:

- Easy enablement: Turn on HappyPay instantly within your Stitch Express account.

- Faster checkout: Customers see HappyPay as an option right at checkout, reducing cart abandonment.

- Cash flow visibility: Merchants can view their balance and transactions on their Stitch Express dashboard.

For merchants already using Stitch Express for payments, enabling HappyPay is the simplest way to add BNPL without juggling multiple integrations. It gives customers more choice while keeping reconciliation, cash flow and reporting streamlined in one place.

Final thoughts: What stores should know

BNPL is becoming an important way for South Africans to pay. For merchants, that means more completed checkouts, bigger purchases and growing revenue. But success depends on choosing the right provider and ensuring a smooth, transparent experience for your customers. Stores that act now to offer BNPL will be better positioned to capture new sales and keep pace with evolving shopper expectations.

Frequently asked questions

What is Buy Now, Pay Later (BNPL) and how does it work?

BNPL allows customers to split their purchase into smaller instalments, often interest-free if paid on time. The merchant receives the full payment upfront while the BNPL provider collects repayments from the customer.

Is BNPL available in South Africa?

Yes. BNPL is growing quickly in South Africa, with services like Payflex, PayJustNow, MoreTyme and HappyPay already serving online and in-store shoppers.

What’s the difference between BNPL and using a credit card?

Credit cards typically involve revolving credit with interest if balances aren’t paid in full. BNPL offers short-term, fixed instalments that are often interest-free, making it more accessible for shoppers who don’t use or qualify for credit cards.

Do BNPL services charge interest?

Most BNPL purchases are interest-free if instalments are paid on time. However, late or missed payments can attract fees depending on the provider’s policy.

What happens if the customer doesn’t pay?

The BNPL takes on all the risk. The merchant still receives the purchase amount.

How do BNPL providers assess credit or spending limits?

BNPL providers use their own checks, which may include credit bureau data, income verification or proprietary risk models, to determine a customer’s spending limit.

How can my business offer BNPL options?

Merchants can integrate with local providers through plugins or APIs for e-commerce platforms like Shopify, WooCommerce or Magento. With Stitch Express, BNPL can be enabled directly from the merchant dashboard using HappyPay.

Which BNPL service is best for bigger purchases in South Africa?

Services like Payflex and PayJustNow are popular for everyday purchases, but HappyPay (via Stitch Express) is particularly well-suited for businesses that want seamless enablement and reliable cash flow visibility when handling higher-value transactions.

What are the steps to start using a BNPL payment option online?

Customers select BNPL at checkout, create or log in to a BNPL account, agree to repayment terms, and complete the purchase. The merchant is paid in full upfront, while the customer repays the BNPL provider in instalments.

Integrate seamless BNPL solutions with Stitch