How does card pre-authorisation work?

Summary: This article explains how card payment pre-authorisation works and why it is essential for industries where final transaction amounts vary. It explores common challenges with traditional pre-auth flows and shows how simplified, automated pre-authorisation improves cash flow, operations, and customer experience for enterprise merchants.

Pre-authorisation (pre-auth) is a fundamental part of payment flows where the final payable amount isn’t known upfront. In card payments, a pre-auth enables merchants to verify whether a customer has sufficient funds and place a temporary hold on those funds before providing a product or service, without actually charging the card yet.

This is common for use cases like car rentals, hotel check-ins, food or grocery delivery, ride sharing and others – where the final cost or transaction amount may go up or down based on incidentals, changes or additions such as tip.

Unlike a standard authorisation, which moves money immediately, a pre-authorisation gives merchants flexibility to settle the final and accurate amount later. But it can be complicated in practice. A clunky set up can complicate operations and frustrate customers.

How pre-authorisation works

- The customer initiates a payment by tapping, swiping, inserting their card, or paying online.

- The merchant sends a pre-authorisation request which goes to their gateway/acquirer and then to the issuing bank (cardholder’s bank).

- The issuer checks for sufficient funds and verifies that the customer has enough balance or credit available for the transaction.

- The issuer places a hold. The funds are not debited and appear as a pending amount on the customer’s account.

- The merchant completes or cancels the request:

- If the goods are shipped or the service is used, the merchant sends a completion (capture) request for the final amount.

- If the order doesn’t go ahead, the merchant releases the hold, or it expires automatically after a set period.

- Settlement takes place after completion. The payment moves through clearing and is deducted from the cardholder’s account.

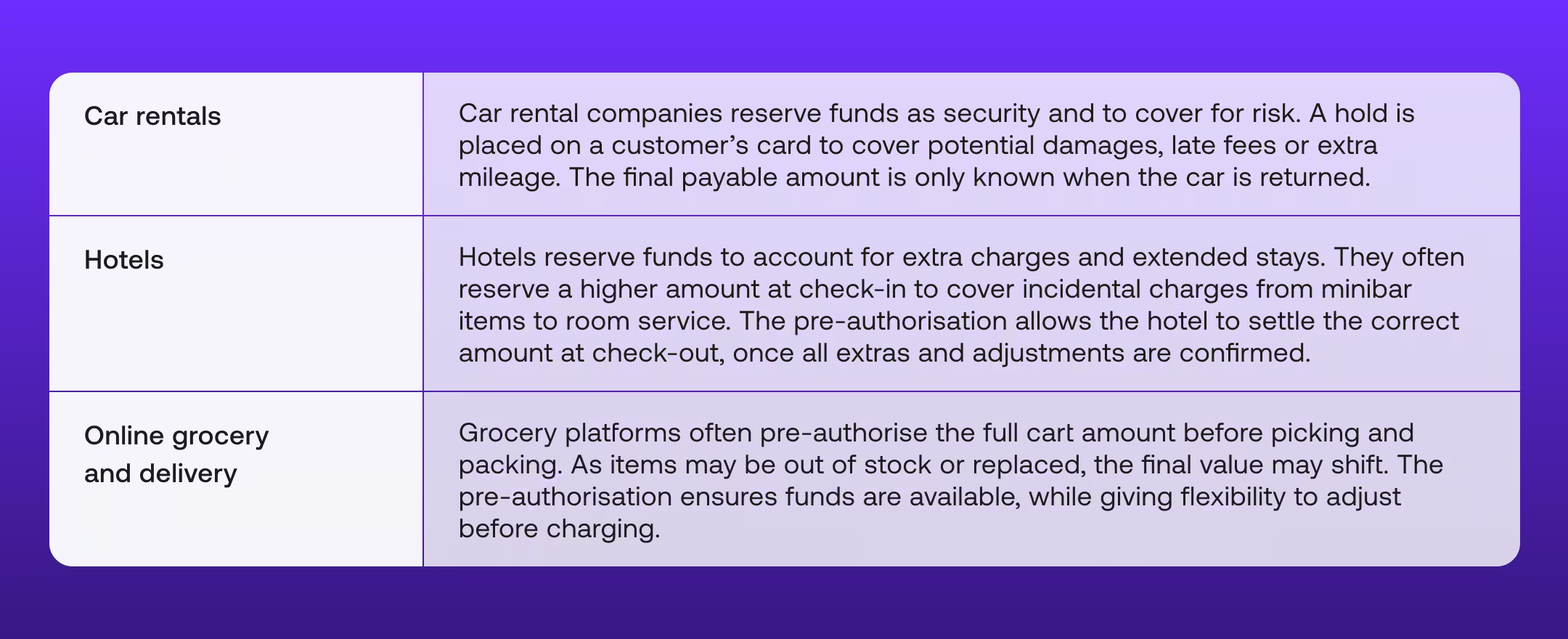

Pre-authorisation use cases

Pre-authorisation is used in industries where prices may shift or additional charges may apply. For example:

Pre-authorisation gives these businesses the control they need to charge for goods and services accurately. However, long waits, manual refunds and unclear holds create friction for both merchants and customers.

Challenges with pre-auth - and how Stitch can help enterprise merchants solve them

A fragmented pre-authorisation setup can slow down cash flow, annoy customers and put strain on internal teams. The Stitch payments platform is designed to remove that complexity.

Long void times affect cash flow

Merchants must claim or cancel a hold within a window specified by their payments service provider. Windows can range from 7 to 30 days. If the funds are unclaimed, standard pre-authorisation holds can take 21 days or more before they are released to the customer. During that time, customers see funds tied up while merchants can’t easily release, adjust or capture the funds until the hold expires.

Stitch gives merchants the flexibility to void transactions within a day or two, improving cash flow management and allowing customers faster access to cash.

Manual refunds slow down operations

Some merchants choose to take the full amount up front and then refund the difference after the order is fulfilled. This takes more time and can be more expensive: Card refunds can take up to 14 days.

Stitch automates refunds and has the capability to payout into a bank account, card, or digital wallet.

Customers must provide bank details for refunds

In traditional flows, customers often need to upload or send their account details to receive leftover or adjusted balances. This adds friction and increases support queries.

Stitch simplifies the workflow by releasing the hold automatically to the original payment method, improving UX and reducing manual errors.

Customers can’t control how much is reserved

Large or unexpected reserve amounts can frustrate customers, especially if the hold exceeds what they can afford or feel comfortable with.

Streamline your pre-authorisation flow

An automated and simplified pre-authorisation flow can improve cash flow, reduce disputes and improve customer trust. Stitch gives merchants the tools to run pre-authorisations that are straightforward and trouble-free, resulting in effortless checkout experiences.

Speak to our team about building smoother, more flexible payment experiences.

FAQs

What is payment pre-authorisation?

Pre-authorisation is a card payment process that verifies available funds and places a temporary hold on a customer’s card without charging it immediately, allowing merchants to settle the final amount later.

How does pre-authorisation differ from standard authorisation?

A standard authorisation captures funds immediately, while pre-authorisation only places a temporary hold. The final charge is completed once the exact transaction amount is confirmed.

Which industries commonly use pre-authorisation?

Pre-authorisation is widely used in car rentals, hotels, online grocery and delivery services, ride sharing, and other industries where prices may change due to incidentals or adjustments.

Why can pre-authorisation be frustrating for customers?

Customers may experience long hold periods, unclear reserved amounts, or delayed release of funds, which can limit access to their money and reduce trust in the merchant.

What operational challenges do merchants face with pre-authorisation?

Common challenges include long void times, slow manual refunds, fragmented workflows, and increased customer support queries related to held funds.

How does Stitch simplify pre-authorisation for merchants?

Stitch enables faster voids, automated refunds, and seamless release of holds back to the original payment method, reducing operational complexity and improving customer experience.

How does improved pre-authorisation impact cash flow?

Shorter void windows and flexible capture options help merchants manage cash flow more effectively while giving customers quicker access to their funds.

Streamline your card payments