A guide to South African payment rails

Payment rails are the infrastructure that keeps money moving. In South Africa, businesses have access to a diverse and rapidly evolving set of rails — from card networks and Electronic Funds Transfer (EFT) to real-time options like PayShap and RTC, as well as emerging methods like crypto and vouchers. This guide explains how each rail works, what makes it distinct and how enterprise businesses can leverage the right combination to optimise their payments operations.

The payments landscape in South Africa has evolved at a rapid pace over the last few years, with more payment methods - meaning more options - than ever before available for businesses to offer consumers. Demand continues to rise from consumers for more choice in how they wish to pay, and access to more seamless and secure payments experiences.

These payment methods are built on top of the payment rails available in the South African market, each of which offers different benefits and experiences. In this guide, we look at the existing payment rails in South Africa, how they work, and how they can meet different needs for enterprise businesses.

What are payment rails?

Payment rails are the infrastructure that allows money to move from one party to another. They encompass the technology, systems, rules, processes and networks that facilitate financial transactions. In essence, payment rails are the conduit that allows money to flow between different organisations and individuals.

There are a number of different payment rails in operation globally, from traditional card networks such as Visa and Mastercard, to automated clearing houses used by banks, to the newer wave of open banking-enabled instant payment networks such as India’s Unified Payments Interface (UPI), Brazil’s Pix and the UK’s Faster Payments Network.

Payment rails can be global or local in nature, and different options might be preferred for different businesses, depending on what their payments needs are and what they’re looking to achieve with different types of transactions.

Payment rails in South Africa

Below is a list of the main payment rails in use across South Africa, including how they work and what makes each one suited to different types of transactions.

Card rails

Card networks are perhaps the most popular of all digital payment rails globally. Visa and Mastercard are the two most popular providers, each with more than a billion cards in circulation.

Card payments have been around for a long time, and many additional or alternative payment methods position themselves as a way to replace card payments, offering faster settlement times, lower fees for merchants and more. However, card rails are still growing in popularity as consumers reduce their reliance on cash and increasingly spend money online – and more convenient solutions such as digital wallets are built on top of card rails and processed over the same networks.

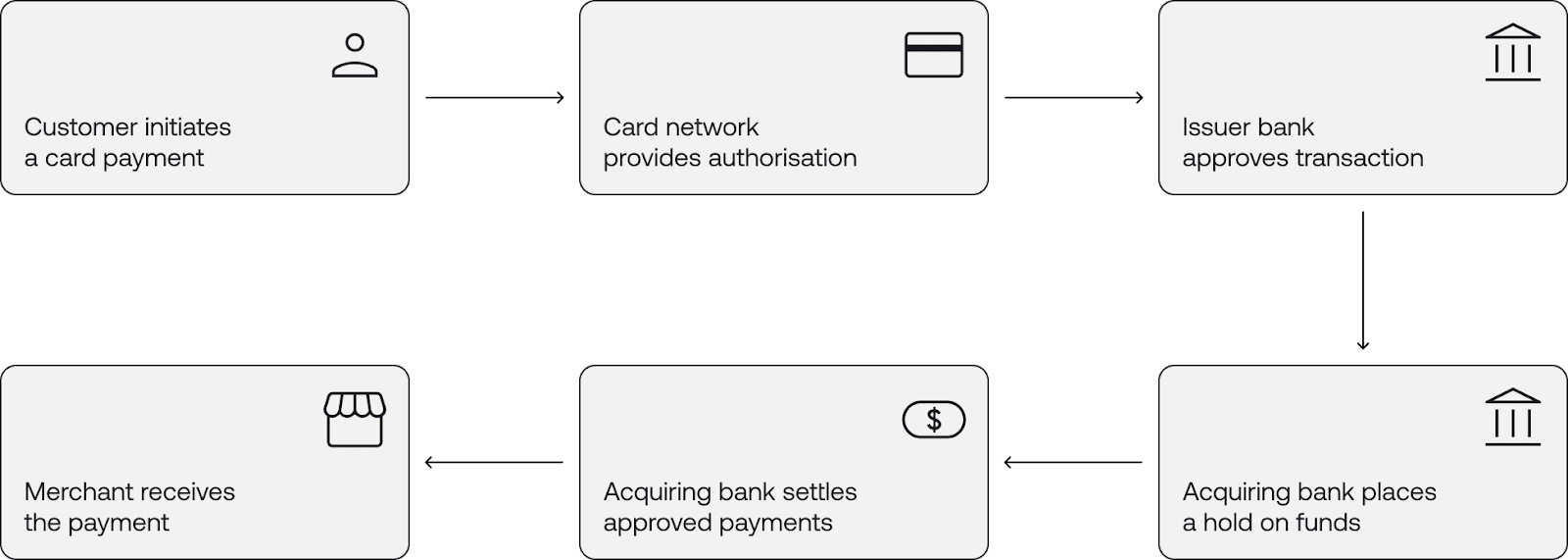

Here’s an overview of how the card payment process works for online transactions:

- A customer initiates a card payment via an online store or service. The merchant’s payment gateway views their card details and communicates with the retailer’s bank (the acquiring bank)

- The acquirer then contacts the issuer to provide approval for the transaction. The issuer will validate the transaction, checking whether the account is valid, whether there are sufficient funds, etc.

- An approval message is sent to the acquirer. The issuer places a hold on the customer’s funds

- Later, often at the end of the business day, all approved payments are transferred in batch to the merchant account. This is known as settlement, and it is at this point that the card network, the issuer and the acquirer charge transaction fees

Card payments generally take between one and four days to clear.

The Stitch Group offers card payments online and in-person; and holds a Designated Clearing System Participant (DCSP) through its acquisition of Efficacy Payments in 2025, enabling the Group to offer end-to-end card acquiring services directly. This vertical integration means merchants working with Stitch can access the full card processing stack through a single partner, improving reliability, cost efficiency and control.

Digital wallets are built on top of card rails and allow consumers to pay using their smartphone, smartwatch or other device rather than a physical card. Stitch launched digital wallet payments in July 2024, enabling merchants to accept Apple Pay, Google Pay and Samsung Pay through a single integration – with no additional complexity for the merchant. For consumers, digital wallets offer speed and convenience, often completing checkout with a single tap or biometric authentication. For merchants, they open up a broader addressable market of mobile-first customers.

Electronic Funds Transfer (EFT)

Electronic Funds Transfer (EFT) is the underlying payment rail that moves money between bank accounts in South Africa. Operated by PayInc, the EFT rail settles transactions in batches rather than in real time, which makes it more cost effective than instant rails such as RTC or PayShap, but slower to clear. As EFT is a rail rather than a product, there are different ways a customer or business can initiate a transaction over it. The choice of initiation method affects the customer experience, the speed of confirmation and the reliability of the payment, even though the underlying infrastructure is the same. The main ways to transact over the EFT rail are Pay by Bank, manual EFT, debit orders and DebiCheck. It is important to note that once an EFT payment clears, it is final and irrevocable.

The two main ways to initiate a traditional EFT are Manual EFT and Pay by bank. Both methods settle over the same EFT infrastructure, but offer meaningfully different experiences for customers and merchants. Manual EFTs require customers to leave the app or website where they’re looking to pay, open their banking app or portal, and manually enter the recipient’s bank details and payment reference. Pay by bank keeps the customer within the merchant’s checkout flow and initiates the EFT programmatically, resulting in faster confirmation and lower drop-off.

With Stitch Pay by bank, returning customers can pay more seamlessly, without leaving the app or site they're on, and can save their bank details to pay in one click whenever they come back to make another payment. The result is a much smoother, faster and more efficient payment experience. Pay by bank transactions also settle in 1-2 days, while Manual EFTs can take 2-3 days.

Here’s an overview of how EFT payments work:

- Initiation

The customer initiates the transfer. This can happen in a number of ways, for example through their online banking app or portal, via bill payment services or by providing payment details over the phone. The payer provides details of the recipient’s bank details such as their account number and a unique reference - Verification

The payer’s bank verifies the transaction details, including the availability of funds and, often, the identity of the recipient. With Stitch, the payer’s identity can also be verified against KYC details stored by the merchant - Transfer

Once the transaction has been verified, the payer’s bank debits their account - Confirmation

The payer and recipient both receive confirmation of the transaction. This often happens through the banking app, via email or by SMS - Settlement

The EFT network clears and settles the funds. This may happen through bulk processing or individually

Once an EFT payment clears, it is final and irrevocable.

A development in South African payments is the emergence of proprietary bank payment APIs, sometimes called open banking APIs. The three live open banking APIs in the South African market are Capitec Pay, Absa Pay and Nedbank Direct EFT – all of which are available through Stitch. These are fundamentally different from EFT in that rather than routing through PayInc’s clearing infrastructure, both initiation and settlement are handled entirely within the bank’s own systems. The customer authenticates and approves the payment natively within their bank’s own app or interface, and the funds move through the bank’s internal ledger. They are best understood as a distinct payment method that sits alongside EFT, not on top of it.

Debit orders and DebiCheck transactions are on the EFT rail, and the primary one used for recurring payments. Unlike the push-based flows above, these are a pull mechanism: the payee is authorised to collect funds from the payer’s account on a recurring schedule, without requiring the payer to take action each time. They run on the EFT rail, and are commonly used for insurance premiums, loan repayments, subscriptions and other recurring billing scenarios. Stitch supports both debit orders and DebiCheck as part of our recurring collections solution.

Real-Time Clearing

Real-Time Clearing (RTC) is a form of instant payment that allows funds to be transferred from one account to another, immediately, and irrevocably. RTC payments are more expensive than EFTs, and are used more regularly for payments that require fast settlement. They are used for lower value transactions (R5 million and below). According to the Payments Association of South Africa (PASA), South Africa pioneered the first interbank RTC payment.

How it works:

- Initiation

The payer issues a payment instruction to the paying bank. This can be done over the phone, online or in a bank branch - Settlement

The paying bank then credits the beneficiary account within 60 seconds

PayInc has indicated its intention to gradually migrate RTC transaction flows onto the PayShap rail as part of its broader infrastructure modernisation programme, with the goal of eventually deprecating the legacy RTC system.

Real-Time Gross Settlement

Real-Time Gross Settlements (RTGS) are used for transactions that are higher value than those sent via RTC (i.e. higher value transactions above R5 million), and that require individual settlements.

As the name implies, settlements within an RTGS system happen as soon as transaction information is received from the sending bank, making them irrevocable. Due to their real-time nature, these payments are not batched.

RTGS is typically used for high-value (over R5 million) interbank transfers of funds, and RTGS systems are often operated by a country’s central bank. In South Africa, the RTGS system is operated by the South African Reserve Bank (SARB).

In June 2021, the SARB launched the RTGS Renewal Programme to improve payment provision for the domestic and regional financial system, enhancing access to payment services.

PayShap

PayShap was initiated by PayInc, in line with the South Africa Reserve Bank’s Vision 2025. RPP allows funds to be transferred from one bank account to another, immediately, on instant rails. Since its launch in March 2023, PayShap has grown significantly, having processed over R100 billion across more than 136 million transactions, with over 4.5 million ShapIDs registered.

PayShap payments are instant, irrevocable, easily accessible and interoperable. There are currently 11 South African banks participating in RPP: ABSA, Al Baraka Bank, African Bank, Capitec, Discovery Bank, FNB, HBZ Bank Limited, Investec, Nedbank, OM Bank, Standard Bank and GoTyme Bank.

In August 2024, PayInc announced a mandatory increase in the PayShap transaction limit from R3,000 to R50,000, effective October 2024. Individual banks may set their own limits up to this ceiling. This significant expansion positions PayShap as a viable alternative to RTC for mid-value transactions, and is part of PayInc’s plan to eventually migrate RTC flows onto the newer, more cost-effective PayShap infrastructure.

PayShap comprises three core services:

- Instant payments

This is a real-time clearing service that enables reconciliation of cleared transactions between participants and facilitates settlement obligations in the SARB settlement system, as well as handling all required reporting - Proxy payments

This allows users to make a payment without the need to enter an account number; they can instead use their associated mobile number or a unique business name (ShapName) as a proxy identifier, referred to as a ShapID. - PayShap Request

This service launched in December 2024 and allows payees (individuals, businesses or informal traders) to request immediate payment from payers across any participating bank. Once a payer approves a request via their banking app, funds clear in real time. Banks participating in the first cohort include African Bank, Capitec, Discovery Bank, FNB, Investec, Nedbank, Standard Bank and TymeBank, with other banks expected to follow.

PayShap Request supports person-to-person (P2P) and person-to-merchant (P2B) payments, and is live with Stitch.

PayInc has also signalled plans to introduce QR codes as an additional PayShap payment method, further broadening how South Africans can initiate real-time payments.

Other popular payment methods that don’t leverage the above rails

Crypto

Cryptocurrencies use decentralised ledger blockchain technology to track transactions and prevent fraud. Crypto is popular in South Africa, with many South Africans showing a willingness to transact using popular cryptocurrencies such as Bitcoin or Ethereum.

Cryptocurrencies can be volatile, with large swings in their value relative to traditional, “fiat”, currencies. Stitch offers Pay with crypto functionality to its clients, enabling them to accept payments in crypto and get settled in fiat currency, without the need to manage the crypto transactions themselves. Stitch and our partner manage volatility risk so our merchants don’t have to.

Here’s an overview of how crypto payments work:

- Before transacting, crypto users must typically set up a digital wallet to hold their funds. This is comprised of a public key - used as an address to receive payments - and a private key, which is used to authorise transactions

- To initiate a transaction, users enter the recipient’s public key and the transaction amount. Their private key then verifies the transaction

- Once verified, the transaction is broadcast to the blockchain network, where it is validated by the computers running the blockchain (known as “nodes”). The record of this transaction is then added to the blockchain network’s public ledger to prevent tampering

- The transaction is then settled directly between users, without the need for intermediaries

Vouchers

Vouchers are a cash-to-digital payment option used by many South Africans, enabling those without a bank account to transact digitally or add funds to a digital account. Vouchers can be used online as well as in physical retail locations.

How it works:

- Customers exchange cash for vouchers in a physical retail location, such as a supermarket or petrol station

- Customers can then enter their voucher number on an app or site to top up their digital wallet

- Once topped up, users can transact, bet or trade using the funds in their digital wallet

Cash at ATM

Similar to vouchers, Cash at ATM allows customers to exchange their cash to pay for digital goods or top up a digital account. With Stitch Cash, users deposit cash at an ATM or bank branch rather than paying through a digital payment gateway. It can be used as a way to pay for online purchases, to top up digital accounts or make other payments such as debt payments, using physical currency.

Here’s how it works:

- Customers choose “Cash at ATM” or “Cash at till” when checking out online

- They receive a unique payment reference - which can be entered when completing the payment at an ATM or bank branch

- As soon as the payment is confirmed, the amount is attributed to the customer’s digital account. They receive a notification that the transaction has been completed

FAQs

What are payment rails?

Payment rails are the underlying infrastructure that enables money to move between parties. They encompass the technology, systems, rules and networks that facilitate financial transactions — in essence, the conduit through which funds flow between organisations and individuals.

What payment rails are available in South Africa?

South Africa has a well-developed payments ecosystem with several rails in operation. These include card networks (Visa and Mastercard), Electronic Funds Transfer (EFT), Real-Time Clearing (RTC), Real-Time Gross Settlement (RTGS), PayShap and proprietary bank payment APIs such as Capitec Pay, Absa Pay and Nedbank Direct EFT. Businesses can also offer crypto payments, vouchers and cash-based options to serve customers without bank accounts.

What is the difference between EFT and PayShap?

EFT settles transactions in batches, making it more cost-effective but slower — typically clearing in one to three days. PayShap is an instant payment rail that moves funds between accounts in real time and is irrevocable once sent. Following a transaction limit increase to R50,000 in October 2024, PayShap is increasingly positioned as a viable alternative to RTC for mid-value transactions.

What is Pay by bank and how does it differ from manual EFT?

Both Pay by bank and manual EFT move funds over the same EFT infrastructure, but the customer experience differs significantly. Manual EFT requires customers to leave the merchant's checkout, open their banking app and manually enter payment details. Pay by bank keeps the customer within the checkout flow, initiates the transfer programmatically and confirms the payment faster — typically settling in one to two days versus two to three days for manual EFT.

What is DebiCheck and when should businesses use it?

DebiCheck is an authenticated debit order system that runs on the EFT rail. Unlike standard debit orders, DebiCheck requires the account holder to pre-approve the mandate via their bank before collections begin. It's best suited to businesses with recurring billing needs — such as insurance, lending and subscription services — where payment certainty and dispute reduction are priorities.

What is PayShap Request?

PayShap Request, which launched in December 2024, allows businesses and individuals to request immediate payment from a payer across any participating bank. Once the payer approves via their banking app, funds settle in real time. It supports both person-to-person and person-to-merchant payments and is available through Stitch.

How do crypto payments work for merchants?

Crypto payments use decentralised blockchain technology to settle transactions directly between parties, without intermediaries. For merchants, accepting crypto can broaden their customer base — but managing volatility is a practical challenge. Stitch enables merchants to accept crypto payments and receive settlement in fiat currency, removing the need to manage the complexity of crypto transactions directly.

What is network tokenisation and how does it differ from pre-authorisation?

Network tokenisation replaces raw card data with a secure token that can be used to charge a customer post-purchase — such as for tips or variable adjustments — without requiring the customer to be present or re-authenticate. Unlike pre-authorisation, which has a time limit (up to 30 days before expiry), network tokens have no expiry constraint. This makes them a powerful alternative in scenarios where the final charge amount isn't known at the time of the initial transaction.

Get a reliable payouts solution, built for enterprise businesses at scale