What is VRP and why does it matter in South Africa and Nigeria?

As open banking innovation continues to gain traction globally, variable recurring payments (VRP) is often seen as the key to its future success. With our ...

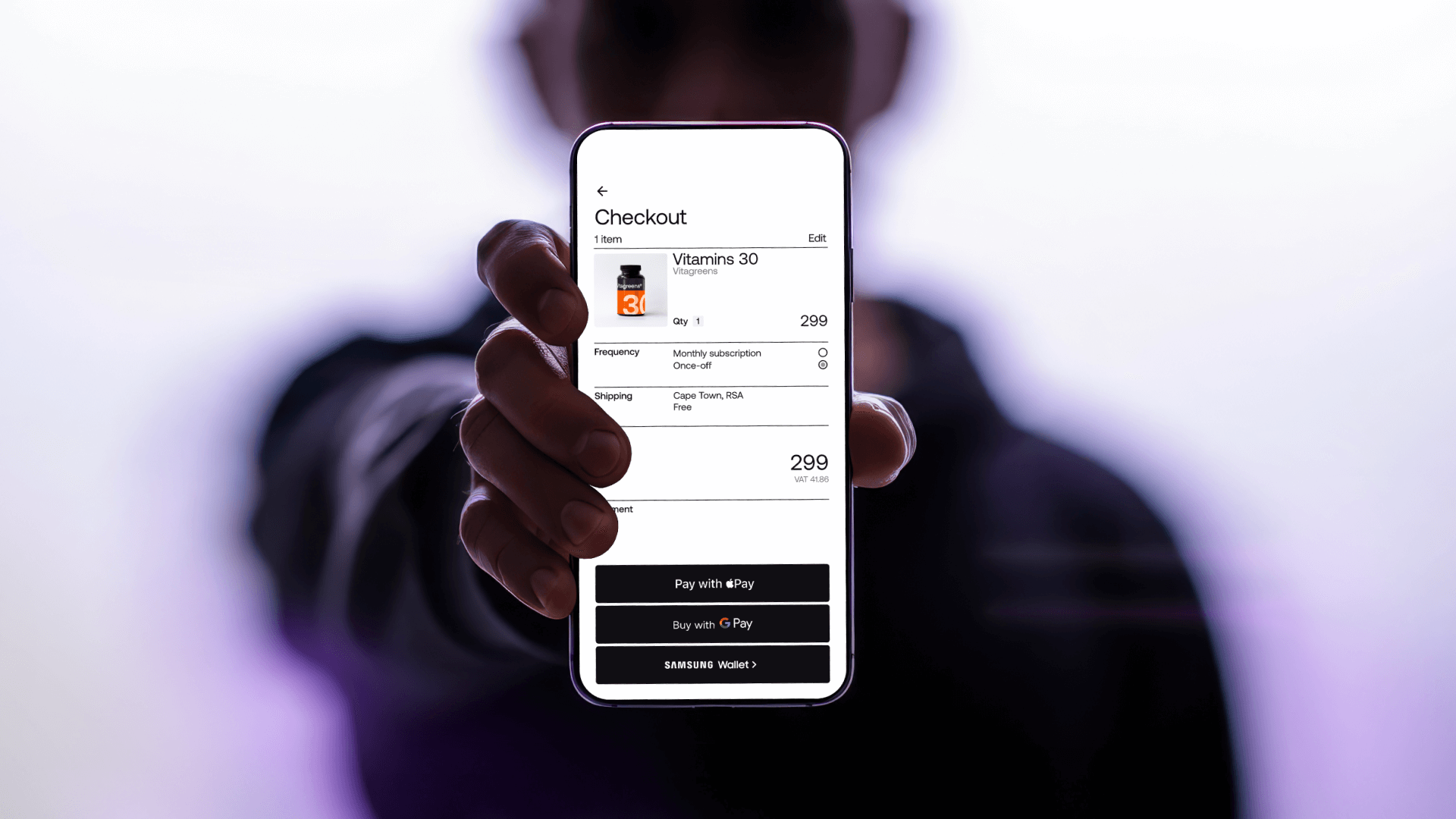

As open banking innovation continues to gain traction globally, variable recurring payments (VRP) is often seen as the key to its future success. With our latest product, LinkPay, we’re able to tokenise user financial accounts, similar to card tokenisation, enabling things like one-click payments and headless payments in which the user does not need to take an action to initiate each payment. This has the potential to be particularly game-changing for African markets, where card penetration remains low, and businesses face high fees and fraud.

What are variable recurring payments (VRP)?

VRP is a type of payment method that enables a consumer or business to authorise a third party to initiate push payments from their bank account on their behalf, according to a set of previously agreed rules and limits.

To understand VRP, it’s useful to understand how it differs from other bank payment methods:

Cards

Compared with cards, VRP is lower cost and has higher conversion (primarily due to 3D Secure customer authentication – a security protocol designed for credit and debit cards to protect online merchants from fraud – and persistence of mandates in the event of lost, canceled and stolen cards). Virtual cards, which expire after a single use, are also increasing in popularity so merchants can find themselves unable to collect on recurring subscription payments.

Debit pull mandates

Debit pull mandates in South Africa and Nigeria are cumbersome to set up and have strict rules around the amount that can be collected and the timing of those collections. VRP can be set up instantly (similar to saving a card on file) and then allows for variable collection amounts and flexible collection timing.

Bank transfers (to a static or virtual account)

VRP can be initiated in the business application with a user present (i.e. the user must take an action to authorise the payment) or via API without the user being present, after the initial mandate is set up. As well, with VRP, users don’t need to manually input recipient bank details, which is often prone to error and fraud.

Payment initiation services

One-off ‘open banking’ payments need to be verified for every transaction no matter the size, so they do not allow for one-click checkout or for collections use cases, which VRP can solve.

Why VRP matters in South Africa and Nigeria

The banked adult population in South Africa is around 75%, and around 45% in Nigeria, while credit card penetration is less than <9% in South Africa and ~3% in Nigeria. By offering VRP as a payment method, businesses can increase adoption of their products by extending their addressable market into previously untapped portions of the population.

VRP as a method is widely applicable across business types. Here are some examples of how the method can improve adoption, cost and conversion for different types of businesses.

One-click e-commerce

VRP allows for a one-click payments experience that doesn’t require the user to possess a card and is still possible even where 3DS has been implemented on credit card transactions. In South Africa and Nigeria, 3DS implementations have made one-click shopping experiences very rare, and merchants often pay significant fees for card transactions. One-click checkouts for returning e-commerce customers that use bank accounts to pay, rather than cards, will lower costs for merchants, improve conversion rates and increase access to a one-click experience.

Online subscriptions

Consumer and small business subscription services often require users to link cards in order for them to sign up. This restricts access to these services for large portions of the population that don’t have cards. With VRP, subscription businesses can now establish mandates easily and at a lower cost, through underlying bank accounts.

In this way, a business can set up the mandate in real time as part of the transaction flow. They no longer need to rely on debit mandates, which in South Africa and Nigeria often involve an onerous and asynchronous setup. It also improves collections, as businesses can accept payments more cost effectively, with higher conversion rates (bank accounts are far less likely to be canceled/maxed out) and with more flexibility, as merchants are not bound by pre-defined collection dates and times.

On-demand services

Many consumer on-demand services such as ride-sharing or food delivery require users to link a payment method (usually a card) as part of the account setup process. Cards can now be replaced with a linked bank account as the preferred payment method during onboarding.

This is a big advantage in South Africa and Nigeria because users that don’t have a card rely on cash-on-delivery to pay for these services. Paying via cash-on-delivery increases the risk for consumers and suppliers in the marketplace and also increases the number of transactions that move off-platform. Using VRP can enable marketplaces to return a greater percentage of their transactions on-platform, increase safety in their ecosystem and enable a much smoother user experience.

We’re excited about the possibilities that can be unlocked with access to this technology. Businesses interested in LinkPay can learn more and get started here.