Why demand for faster digital payment channels is increasing in Africa

How people pay for services and goods has never remained static. Businesses and individuals have always tried to move money faster. Since the first electronic

How people pay for services and goods has never remained static. Businesses and individuals have always tried to move money faster. Since the first electronic money transfer transaction was completed by the Western Union Telegraph Company in 1871, electronic, and subsequently digital payments, have become a core part of how we pay for the things we buy.

As consumers continue to demand more speed, convenience and security in the way they make a payment, these payment methods need to be faster, more convenient and even more secure. Africa currently leads global growth in the adoption of digital payment alternatives.

Making fast, even faster

In response to increasing demand from consumers, more merchants plan to accept digital payments and pay their suppliers digitally, bypassing cheques and other more manual payment methods. The number of global non-cash transactions grew by six percent from 2019 to 2020, and the pandemic only accelerated that shift in consumer spending behaviour, with projections of non-cash transactions globally hitting 1.8 trillion by 2025 at a compound yearly growth rate of 18.6%. According to McKinsey, instant payment infrastructure will give additional impetus to growth, and Africa will contribute significantly.

B2B payments are also not left out. According to Capgemini, by 2025, global B2B non-cash transactions will increase by almost 61% to nearly 200 billion from 2020 levels. As more people make digital payments, customers can now choose from different payment methods, all of which vary in speed, ease, cost and security.

This change is not just happening in developed markets. Propelled by an increase in smartphone use and improvement in internet access and connectivity, the adoption and indeed demand of digital payment channels in emerging markets, especially in Africa, is now outpacing growth in the adoption of digital payments in Europe, for example. For this reason, secure, instant transactions will become an even more important part of user experience design.

Of course, developed economies have had decades to implement more conventional cashless payment infrastructure, which is primarily based on credit cards. These legacy structures now hamper the adoption of newer and faster payment channels in these markets.

But this infrastructure has failed to scale in African markets, as penetration of card both on the merchant side and consumer side has been relatively slow. Card payments are costly for merchants and require necessary infrastructure to accept. Many consumers struggle to access cards, and as a result, Africa is playing a big part in the shift that prioritises faster and more secure non-card digital payments.

In markets like Nigeria, for instance, the growth of instant digital payments compared to card payments or mobile Point-of-Sale (mPoS) has been dramatic. In the first two months of 2022 alone, almost $130 billion (₦53.83 trillion) was transferred through Nigeria’s instant payment system, compared to only $2.7 billion (₦1.15 trillion) processed through PoS terminals. According to Nigeria’s Central Bank Data, online transfers constitute around 57% of the total volume of online transactions made between January and August 2020. What is driving this growth?

- More Africans have bank accounts than have credit or debit cards.

- Rising smartphone penetration is enabling more, and more convenient, access to digital payment methods.

- Instant bank transfers bypass some of the high fees and operational costs associated with other e-payment channels.

- Instant payment options settle faster than alternatives such as card payments, meaning that merchants are able to access funds from sales revenue faster.

- Instant bank transfers are more convenient than other payment options, improving conversion rates for merchants and reducing friction for consumers.

- Instant payment solutions like Stitch are built with fraud prevention in mind and are less risky compared to using credit cards.

Instant bank payments in Nigeria

Africa’s biggest market in many different ways is also a leader in the adoption of digital payments. The foundation of Nigeria’s instant payment culture was laid in 1992 when the Bankers Committee introduced the Nigerian Interbank Settlement System (NIBSS), a shared-service infrastructure to facilitate payment finalities, inter-bank settlement and promote electronic payments in the country. Jointly owned by Nigeria’s central bank and all deposit money banks, NIBSS serves as the rail system upon which Nigeria’s instant banking and payments infrastructure runs as well as the gatekeeper of Nigeria’s banking and finance sector.

As a result of this, fast bank transfers are not only expected in Nigeria, they are demanded. Last year alone, NIBSS recorded 3.1 billion in instant payment transactions, valued at $582 billion (₦241.7 trillion). This is a 75% increase in transaction value from 2020 and a 74% increase in the number of instant payment transactions compared to 2020. It is also the strongest evidence of how payment behaviour is decidedly moving online. In the first two months of 2022, instant bank transfers totalled close to a quarter of last year’s total transactions.

Despite the growth, instant digital payments in Nigeria are still very manual. Consumers have to log in to their bank every time or dial complex USSD codes to make simple payments. In a country where 45% of the population are banked, versus only 3% credit card ownership, merchants who offer convenient and secure bank payments will improve the experience of their customers and increase reach, conversion and retention.

Source: Nigeria Central Bank

The rise of instant bank transfer in South Africa

Despite being one of Africa’s earliest adopters of real-time clearing (RTC), South Africa, unlike Nigeria, has been slow to unlock the value of instant interbank payments despite its large banked population (70%–80%). But attitudes among consumers, merchants and regulators are changing as merchants and customers continue to demand faster, safer and more convenient ways to pay. This is underlined by the continued growth of PSPs and payments aggregators in the market, including Peach Payments, Zapper, SnapScan, Yoco and many others who are working to enable merchants to accept digital payments for the first time – with more options for the consumer than ever.

While card payments represent one piece of the digital payments evolution, merchants and consumers face challenges with this method, including rising fraud, expensive fees and chargebacks. In 2020, card fraud in South Africa increased by more than 26.5% to R520.5 million, inevitably decreasing merchant confidence in card transactions. As a result, South African customers are demanding faster interbank transfer channels.

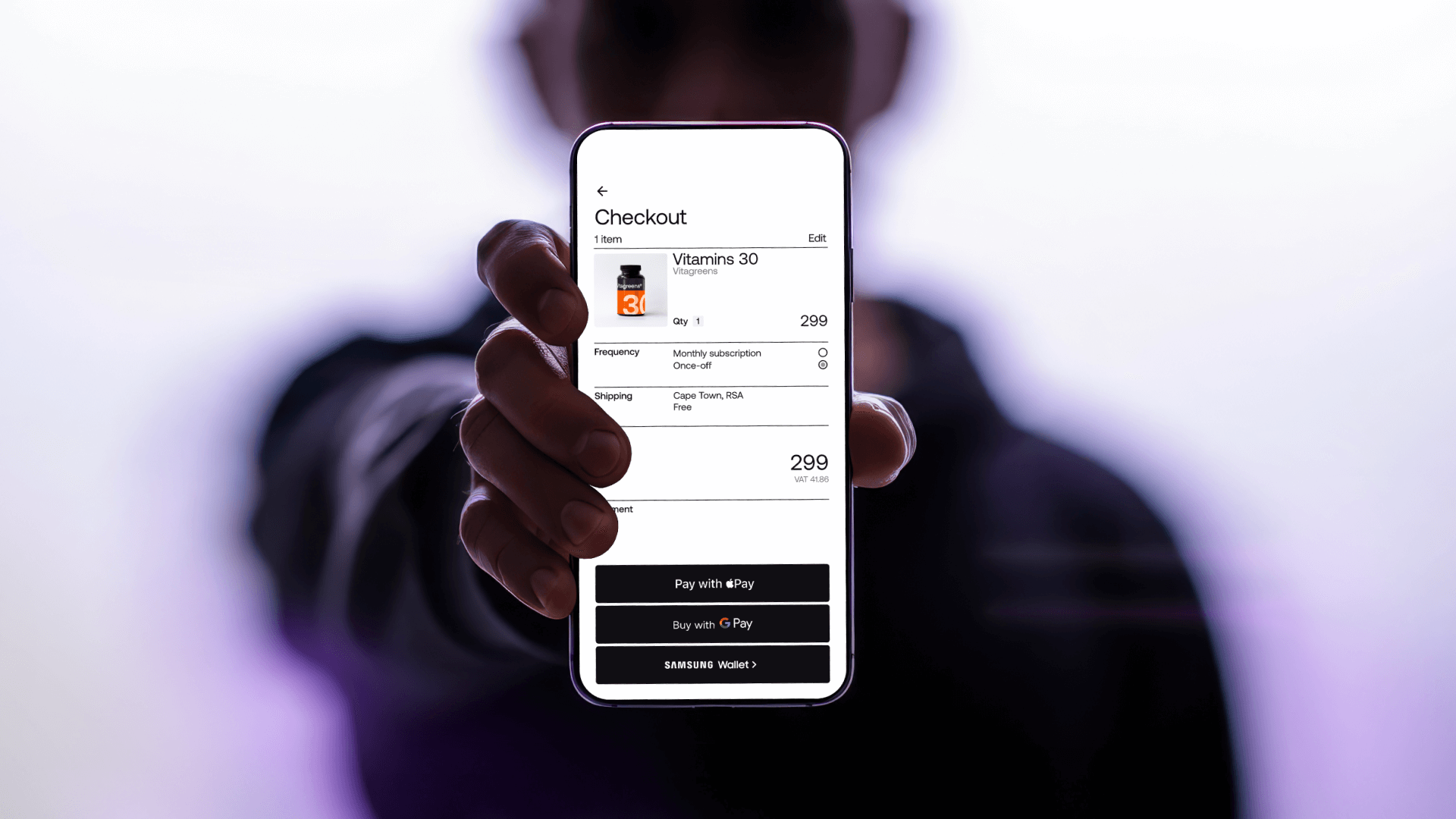

Stitch’s instant EFT solutions, LinkPay and InstantPay, make it easy for merchants to accept fast, secure bank transfer payments that are also significantly cheaper compared to the existing standard electronic funds transfers, card payments or other digital alternatives. This also allows merchants to safely provide a payment option that is convenient, and that customers want, while reducing the costs of accepting digital payments.

With about 70% of South Africa’s adult population having a bank account, versus only 9% with a credit card, it only makes sense to leverage bank transfers and make them faster and safer so that customers have better options to make digital payments without needing a card to do so. And this is exactly what Stitch has done.

According to a Deloitte study on the future of payments in South Africa, instant payment options like Stitch demonstrate:

“The sweet spot that can be achieved when innovative technologies like instant payments with overlays combine with mobile technology, bringing in fintech players with customer-serving front-end applications, connecting to traditional banking services through APIs, and accessing the real-time payment system to deliver the payment instantly. This brings speed and efficiency into everyday transactions, building trust and reliance on alternatives to cash and ultimately supporting financial deepening.”

In other words, merchants build trust and loyalty when they offer payment options that allow the consumer to choose to securely pay from their bank accounts, bypassing card and other e-wallet fees and the associated fraud risk. Financial service providers can also leverage Stitch technology to support small businesses—even those in the informal sector that depend on easy access to funds from their sales— to offer and accept digital payments.

What’s ahead: the future of instant digital payments in Africa

In sub-Saharan Africa, payments of any kind, digital or not, is a fast, fast game. In a region where trust is low, and informal businesses make up the bulk of the economy, being able to pay for groceries, bills or government services instantly is very important.

For merchants, instant bank transfer payments mean that the merchant is able to immediately access funds from sales, reduce the risk of fraud complaints or chargebacks and cut credit/debit card costs. Besides, allowing customers and users to initiate instant bank transfer payments without leaving the checkout flow—as is the case with USSD payments for example—means less cart abandonment and an overall improvement in the payments experience no matter which vertical your business operates in.

A combination of government reforms, changing consumer behaviour and new technology has contributed to a new appetite for alternative-to-cash payment channels. Besides, more people are shopping online and using the Internet, from their mobile and smartphones. If there is a broad lesson from the rise of digital payments in Africa, it is that the push to increase the banked population and simplify banking transactions will lead to an increase in demand for fast bank transfer payments that are cheaper compared to debit/credit cards, debit orders, or carrying cash.

Stitch empowers businesses with a simple API that enables them to build powerful financial products quickly, and accept secure and instant payments. Start building with Stitch for free here.