What is South Africa’s Rapid Payments Programme (RPP)?

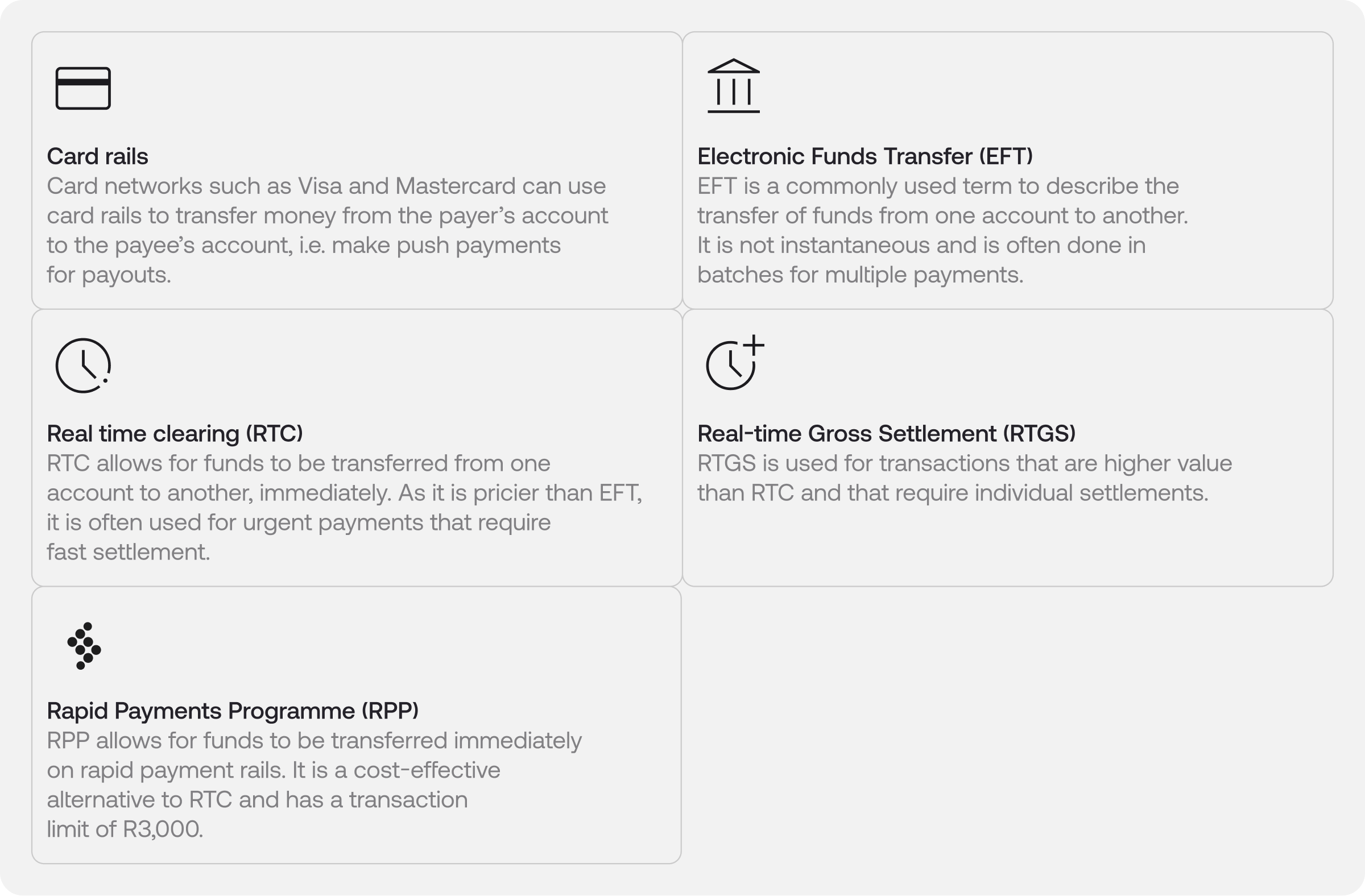

The way we send payouts has been in desperate need of an upgrade. Previously available payout rails and processes were either instant and expensive - or only allowed settlement in a couple of days. Stitch Strategic and Product Partnerships Manager Ujjal Valjee shares a brief summary of the existing rails in the South African market, including where RPP fits in, and how Stitch leverages all available rails to fuel more reliable payouts.

The Rapid Payments Programme (“RPP”) was initiated by BankservAfrica and introduced in line with the SARB’s Vision 2025. PayShap is the brand name of the peer-to-peer marketed products that are a part of RPP. PayShap payments are made on the modernised rapid payments rails introduced with RPP and can be compared to real-time payments seen around the world, such as UPI from India and Pix from Brazil.

Whilst pay-ins and person-to-person payments have been the focus for RPP thus far, the importance of a high-quality payout payment method for businesses is equally important and often underestimated. Payouts as a payment type has long been in desperate need of an upgrade, as the payment methods and rails previously available were either instant and expensive, or only allowed settlement in a couple of days. Today, there is a significant opportunity to utilise RPP for more efficient payouts.

A brief summary of the existing rails and systems that can be found in South Africa provides some context on where RPP fits in the market:

Benefits of the Rapid Payments Program

RPP offers instant, irrevocable payments, with modernised messaging and build. As it was built with a goal of displacing cash, it is cost-effective, easily accessible and interoperable.

Another feature of RPP is the ability to pay by proxy. Pay by proxy means that users do not necessarily have to use an account number to make a payment, as is needed for EFT or RTC. Instead, they can use a cellphone number. The third service, which is still to be released, is Request to pay. This is expected to be a game changer for RPP and will allow the payee to request a payment from the payer.

Interoperability is key for RPP, and its success is highly dependent on mass adoption by the banks in South Africa. As of today, the participating banks are ABSA, African Bank, Capitec, Discovery Bank, FNB, Investec, Nedbank, Sasfin, Standard Bank and TymeBank. These banks, together with BankservAfrica, manage RPP, and are responsible for releasing new features and managing the payment limit.

Whilst the rail is built with the features identified above, RPP's uptime and capabilities are dependent on each participating bank. This is because each bank has its own integrations and focuses on differing features in line with its individual strategy. This means that each bank will have different processing times, might not be available 24/7 365 and may not offer proxy options. The banks also work independently when it comes to how and when they want to release new features as they become available from BankservAfrica.

Fuelling faster, more cost-effective payouts

In line with building a safe, reliable and effective National Payments System that can be used by all, there is a massive opportunity for businesses to utilise RPP for payouts, including refunds, withdrawals from digital accounts and disbursements. It is extremely quick: from payment initiation to settlement, a payment can be processed in a matter of minutes, sometimes even seconds. It is also more cost-effective and incredibly secure compared with other rails.

These qualities make for a great user experience, especially when it comes to payouts, where speed (often, instant gratification) and reliability are key. This helps businesses build trust with their customers and provide a superior service, with little to no additional work required. As RPP was built to facilitate a large number of transactions, high volumes are easily accommodated. As a security measure for this new payment system, the maximum amount allowed to be transferred currently is R3,000. These features, coupled with the low cost of the rail, make it very attractive for facilitating high-volume, low-value transactions.

Stitch has addressed the industry's need for a high-quality payout solution by leveraging RPP’s capabilities alongside other payout rails, to ensure reliable and efficient payouts. Our key to providing this service is having direct integrations into multiple banks and rails, which allows Stitch to automatically route each transaction via the most optimal journey.

Key features of Stitch Payouts include:

- 24/7 365 payouts (avoiding banking maintenance downtime)

- Choice of instant or same-day settlement

- Reliability in the form of multiple redundancies and fallbacks

- Fraud reduction using Stitch Bank Account Verification Service (BAVS)

- Float management

- Ability to manage payout statuses in real-time

The result is an advanced Payouts Orchestration engine that can prioritise between performance, speed, reliability and cost, dependent on what the merchant's needs and goals are.