The anatomy of an African fintech’s tech stack

Wallet, P2P payments + remittances solutions It takes a community to enable a fintech to thrive. We took a look at what a typical “fintech ...

Wallet, P2P payments + remittances solutions

It takes a community to enable a fintech to thrive. We took a look at what a typical “fintech stack” might look like for a wallet business launching in African markets, and how various solutions work together to help one another succeed.

Fintech and embedded finance businesses are launching and expanding on a near daily basis in Africa – meaning more and more innovative solutions are reaching African customers. Today these businesses are able to get up and running, and expand to new markets, more quickly than ever, thanks in large part to the increasing number of companies that are building critical infrastructure and enabling solutions.

So what exactly does a typical stack look like for a fintech company launching in African markets? How many other products and services might they rely on to launch quickly achieve their vision?

We’ll start by looking at an example of the spectrum of integrations and partners a typical wallet solution might rely on, in Nigeria and South Africa.

The stack

As described in Samora Kariuki’s Frontier Fintech Newsletter, a wallet solution like Chipper Cash, for instance, “gets licensing in each market, partners with someone for identity verification, opens bank accounts for store of value and negotiates exchange rates for settlements. It then partners with a player such as Flutterwave for centralised liquidity management, reporting for some payment types and payments and collections for some markets.” For some solutions, such as Bankly, the stack extends beyond tech and involves a network of physical agents that act as the final touchpoint with end users.

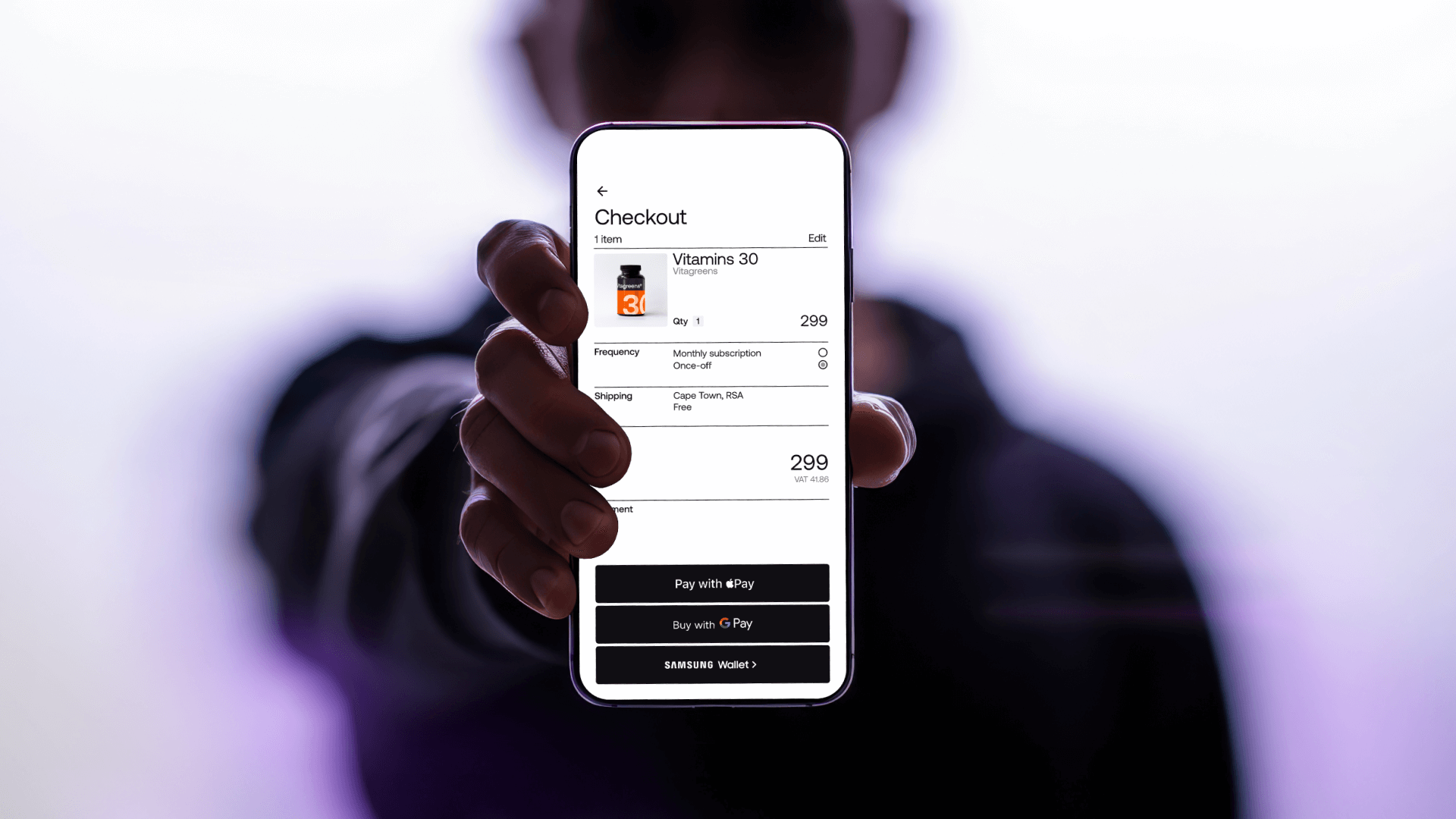

Stitch was built to alleviate some of the infrastructure challenges that businesses face by connecting – or stitching together – the various nodes that constitute the continent’s financial graph. We do this by integrating with major banks, wallets and financial institutions to enable our customers to offer pay-ins and payouts, provide robust onboarding and anti-fraud capabilities, enable access to user bank account data, and overcome regulatory hurdles in each market.

Innovative players across the ecosystem are each tackling their own piece of the stack. Here’s a look at some of the integrations and partners that a wallet business launching in South Africa or Nigeria might rely on.

South Africa

Nigeria